- SELLING RESOURCES -

Reviewing offers

With YELLOW, it's easy to understand an offer and compare it to other offers.

- THE OFFER -

The offer is not just a sale price you receive from a buyer – there are many parts to the offer and a lot of items to consider.

In addition to the price, you'll have to consider things like the deposits, the financing type, timeframe, and any contingencies.

Fortunately, YELLOW has made the offer easy to understand and easy to accept, reject, or counter.

YELLOW MAKES THE OFFER EASY

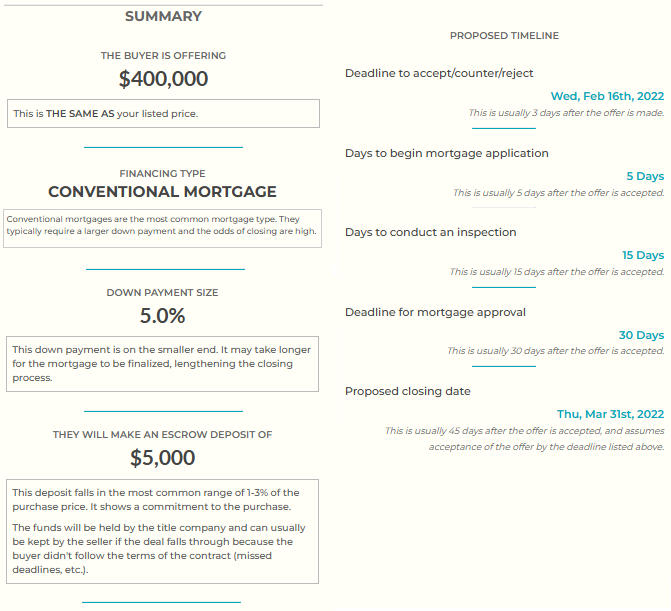

OFFER SUMMARY

The offer can be complicated. It comes on a legal contract that is a dozen pages long and filled with legal jargon.

To make it easy, YELLOW provides a summary of the offer and a guide to help explain the contract in full.

Here's an offer summary the seller will see:

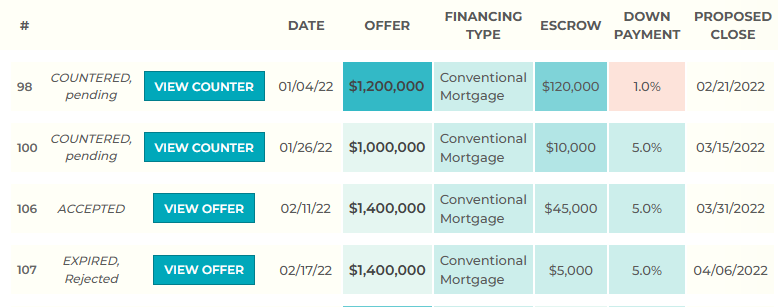

COMPARE MULTIPLE OFFERS

YELLOW provides a color-coded summary of all offers for easy comparison.

The purchase contract is filled with legal-speak and can look intimidating on its own. For that reason, we've created a 'Purchase Contract Guide' that provides explanations for each section. It's linked below:

Sellers can also check out our guide to the purchase contract from the sellers perspective. This looks at things like deadlines and conditions strictly for the seller.

Don't forget, YELLOW is here to help and can walk through any form with you.

ADDITIONAL RESOURCES

- PARTS OF THE OFFER -

We'll discuss the main sections of the contract below.

SALE PRICE

This is the most important part of the offer. Did the price come in at or near your goal? See how much you will walk away with using a calculator.

CONTINGENCIES

These are the things that must be completed or satisfied before the deal can be closed. They are for the benefit of the buyer - if they aren't completed or if they reveal a problem, the buyer can back out of the deal and keep their earnest money.

COMMON CONTINGENCIES

Inspection

You have already completed an inspection that YELLOW has provided for the buyer. However, the buyer can do their own, if they choose.

The buyer can walk away from the deal if an inspection reveals a problem that they don't feel comfortable with. This could be any inspection - from the general inspection to the WDO or lead paint or septic or any other inspections that may have been completed.

Appraisal

An appraisal will be required for buyers using a mortgage.

If the appraisal comes in below the amount you agreed on, it will give a reason for the buyer to try to renegotiate the sale price. If a deal isn't reached, they can cancel the contract. This is usually only if the appraisal is significantly below the sale price - slightly below is often acceptable.

Financing

Even though the buyer has a preapproval for a mortgage, they may not be ultimately be approved for a mortgage. Without financing, the deal falls apart and the buyer can exit without penalty. This is the most common reason for deals falling through.

Title

If there turns out to be a problem with the title, the buyer can cancel the deal.

Keep in mind that these, too, are all a part of a negotiation. If you don't like the contingencies, you can simply reject the offer or make a counter offer.

ADDITIONAL RESOURCES

FINANCING METHOD

The offer will include how the homebuyer will finance the home purchase. This is important because it gives you an idea how long it will take to close.

CLOSING DATE

This is the date the buyer plans on closing. Closing quickly may sound great, but remember you must have a new place to live and need time to pack. Ideally, the closing date should suit both the buyer and seller.

The average closing time is around 45 days and most close between 30-60 days (what is the buyer doing during the closing process? Find out HERE). Have realistic expectations for closing times.

EARNEST MONEY

This deposit is the amount the buyer will pay into an escrow account to show that they are serious about their offer. It's most common to see a deposit of 1% - 2% of the purchase price, and usually a round number in that range, like $2,000 or $4,000. Homes on the lower end are usually closer to 1%.

If the buyer fails to follow through on certain parts of the contract before closing, the seller will likely be entitled to that money.

Visits to your home

Accept offer